Halal Income Stock: A Hong Kong Native, Henderson Land

This Asian large-cap has been paying a high dividend through the market ups and downs.

The Chinese stock market has been cheap for a good few years now, hence the abundance of high dividend payers. But sifting through them for quality companies, let alone halal tayyib stocks, is far from easy.

Looking for more halal dividend stocks?

The property sector is traditionally aligned with Islamic financial principles and therefore a ready place to start. Part of the FTSE Hong Kong and China Shariah Indices, Henderson Land is a leading property developer in Hong Kong and Mainland China and a Shariah compliant business for Muslim income investors to consider.

Henderson Land Development (SEHK:00012)

Sector: Real Estate

Market cap: HK$114b

Net margin: 39.6%

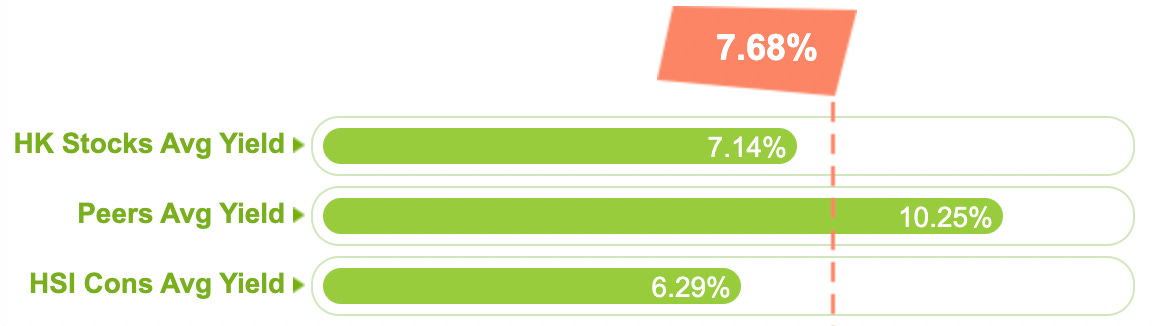

Dividend yield: 7.68%

Price/Earnings ratio: 10.4x

With COVID-19 and property sector troubles in China, it has not been smooth sailing for Henderson Land. But despite a low revenue growth rate (of about 2% per annum) and declining earnings, the company has maintained a stable dividend return to shareholders of HK$1.8/share over the past five years. Though, naturally, that required increasing the payout ratio: from under 30% in 2018 to more than 80% in the latest financial year.

A definite positive is the future outlook. Earnings are expected to grow 8.6% per annum over the next three years. Cash flows — 63% of which are currently being used to cover dividend payments — will subsequently be boosted. Already for the first six months of 2023, net profit rose by 18%. Revenue is projected to continue to inch up, by 2.5% per annum.

Importantly, the management is committed to sustaining the current dividend levels: the yield is forecast to stay around a high 8% in three years’ time.

The caveat

Earnings trend aside, do take note of Henderson Land’s balance sheet and its extensive use of debt. Total debt, at HK$151b as of end-June 2023, increased by 56% in the last five years. Even so, the company is able to comfortably service debt, with earnings (before interest and tax) almost 6 times interest payments.

Halal high yielder

The analysts are divided on the company. The average price target one year from now is HK$22.66 which implies a -2.4% downside from the current price of HK$23.20. The price-to-earnings ratio of 10.4x is fittingly expensive versus both peers and the industry (6.1x). The stock is thus presumably fully valued at present. But, regardless of the point of entry, the fact remains that Henderson Land is an established high yielder that as a halal income stock deserves a spot on Muslim investors’ watchlists.

Disclaimer: Nothing you read on Tayyib Finance constitutes financial advice. Nor is there a guarantee of Shariah compliance of any particular stock at any particular time, since ‘Shariah compliance’ is fluid depending on the provider of judicial opinion and must be regularly affirmed. Do your own research.